Personal Finance

Public Pension, Occupational Pension, and Private Savings: A Comparison in the Swedish Context

October 7, 2025

7 minute read

The Swedish pension system is structured as a pyramid consisting of three distinct yet interconnected parts: the public pension (allmän pension), the occupational pension (tjänstepension), and private pension savings (privat pensionssparande). Understanding the unique function, funding, and return potential of each of these components is a fundamental prerequisite for designing a robust and sustainable long-term pension strategy. Many savers lack a clear picture of how these parts interact, leading to suboptimal decisions and a potentially lower future standard of living.

Successful pension planning is not built on relying on a single part of the system but on strategically optimizing and combining all three. This analysis provides a structured comparison of the three pillars of the Swedish pension system. We will dissect their mechanisms, highlight their differences, and offer concrete strategies for how you can maximize your total pension income through an integrated and proactive approach.

To optimize your pension, you must first understand the structure and purpose of each individual part. Each component plays a specific role and is funded in a different way.

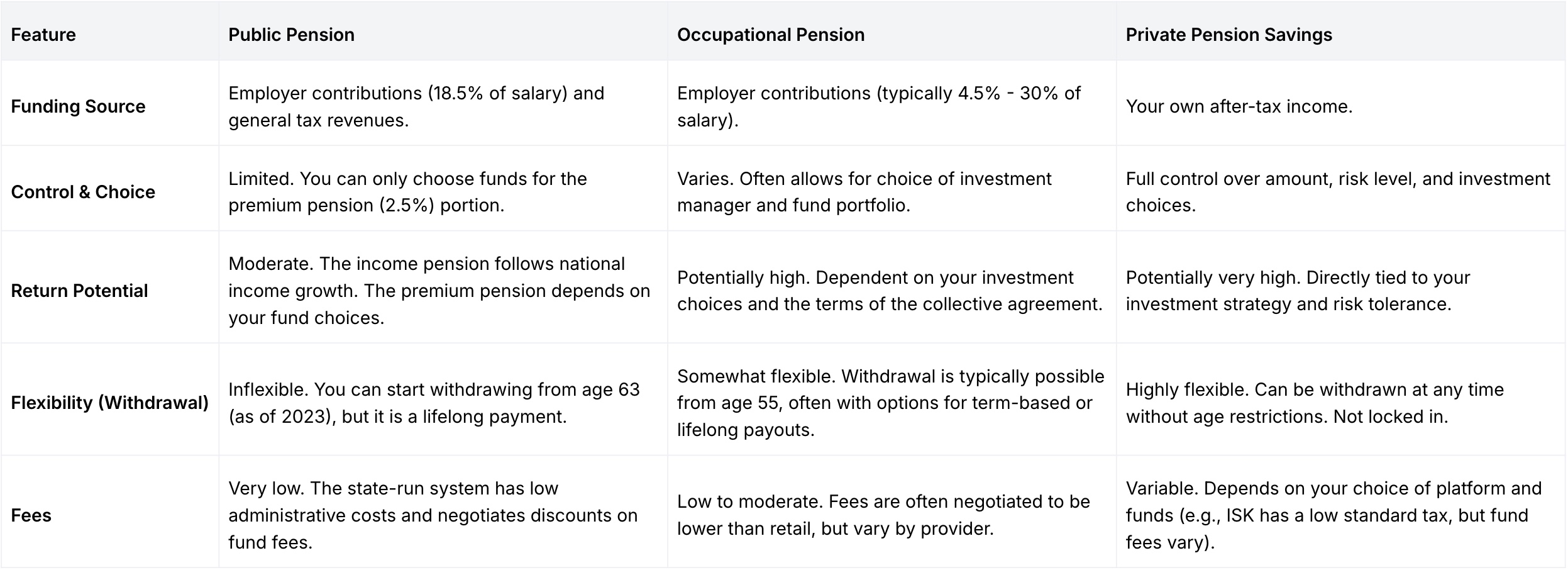

The public pension forms the base of the pension pyramid and is the state-run system to which everyone who works and pays taxes in Sweden is entitled. The system is administered by the Swedish Pensions Agency (Pensionsmyndigheten) and is funded through the social security contributions that your employer pays (or that you pay yourself as a self-employed person). Each year, 18.5% of your pensionable income (up to an income ceiling) is allocated to your public pension.

The public pension consists of two parts:

The occupational pension is the part of your pension paid by your employer. It constitutes an increasingly important part of the total pension, especially for middle- and high-income earners. Approximately 9 out of 10 employees in Sweden have an occupational pension through a collective agreement between trade unions and employer organizations. The size of the contribution varies between different agreement areas but is often 4.5% of the salary up to a certain limit, and significantly more (often 30%) on salary portions above that limit.

The occupational pension can be either defined-benefit (you are guaranteed a certain percentage of your final salary) or defined-contribution (the size of the pension depends on the contributions and the investment returns). The defined-contribution model is now dominant, and here too, you often get to choose how the money is invested.

Private pension savings consist of money that you yourself choose to save for your future pension, beyond what the state and your employer set aside. Since the tax deduction for private pension savings was abolished for most people, the form of saving has changed. Today, private pension savings are primarily done through an Investment Savings Account (Investeringssparkonto, ISK) or a capital insurance policy (kapitalförsäkring, KF).

This is the most flexible part of the pension. You decide how much you want to save, what risks you want to take, and when you want to start withdrawing the money. This part is entirely dependent on your own discipline and your investment decisions.

The optimal pension strategy involves making the three parts work together. It is not a matter of "either/or," but "both/and."

Securing a comfortable pension is not a passive act but the result of conscious and strategic decisions. The three parts—public pension, occupational pension, and private pension savings—together form a powerful system, but only if you actively manage them. By understanding their unique characteristics and how they interact, you can transition from being a passive recipient of your future pension to becoming its architect. A disciplined and integrated strategy, where you optimize each component based on your unique circumstances, is the most effective path to financial security in the future.

How to Maximize Your Pension in Sweden

Salary Exchange in Sweden: Is It the Right Strategy for You?