Finance Terms

What is an Income Statement?

See video transcript

The income statement, also known as the profit and loss (P&L) statement, is one of the three core financial statements that form the foundation of corporate financial reporting. It provides a detailed summary of a company's revenues, expenses, and resulting profit or loss over a specific period, such as a quarter or a fiscal year. Its primary function is to articulate a company's financial performance and operational efficiency.

For investors, analysts, and business leaders, the income statement offers a clear narrative of a company's ability to generate profit from its operations. Alongside the balance sheet and the cash flow statement, it provides the critical data needed for a comprehensive analysis of a company's financial health and valuation. Understanding its structure and implications is a fundamental skill in financial analysis.

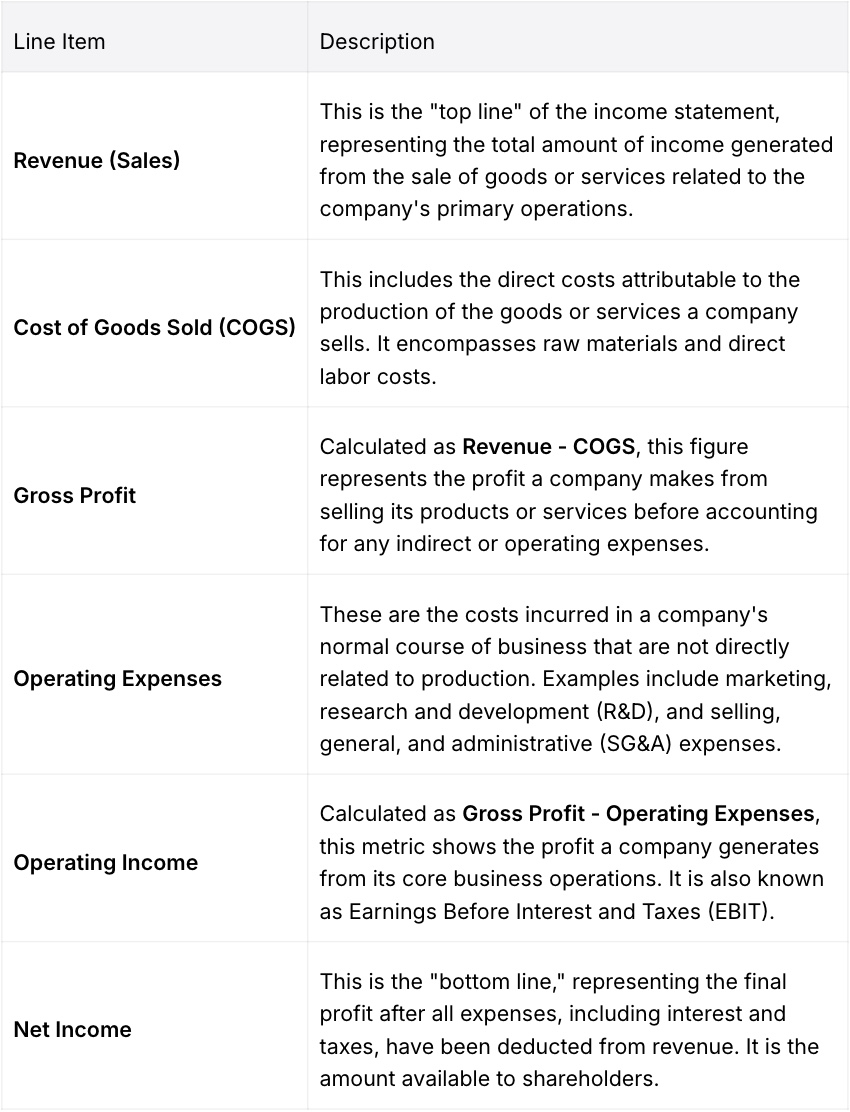

The income statement presents a company's financial journey from its total revenue down to its final net income. This top-down structure allows analysts to systematically deconstruct a company's profitability at various stages. The statement logically subtracts different categories of expenses from revenues to arrive at the bottom line.

Each line item on the income statement reveals a different aspect of a company's performance. The standard structure is as follows:

The income statement is an indispensable tool for investors seeking to evaluate a company's profitability and operational efficiency. By analyzing the trends in revenues and expenses, an investor can gain significant insights into a company's competitive position and future prospects.

First, the statement provides a clear measure of profitability. Key metrics derived from it, such as gross margin, operating margin, and net profit margin, allow for a detailed analysis of a company's ability to convert revenue into profit. Comparing these margins over time and against industry peers reveals whether a company's profitability is strengthening or weakening.

Second, the income statement is crucial for identifying trends. Consistent year-over-year revenue growth can signal strong market demand and effective sales strategies. Conversely, rising costs relative to sales may indicate operational inefficiencies or increasing competitive pressure. Analysts scrutinize these quarter-over-quarter and year-over-year changes to assess a company's momentum.

Finally, the income statement is a primary input for financial modeling and valuation. The net income figure is the basis for calculating earnings per share (EPS), one of the most widely used metrics for assessing corporate value. Analysts use historical income statement data to forecast future earnings, which is a cornerstone of stock valuation.

While powerful, the income statement has limitations that a discerning analyst must consider. Its reliance on accrual accounting principles means that revenues and expenses are recorded when they are earned or incurred, not necessarily when cash changes hands. This can create a divergence between reported profit and actual cash flow.

A company might report strong net income but have negative cash flow if its customers are not paying their bills in a timely manner. Non-cash expenses, such as depreciation and amortization, also reduce net income without an actual cash outlay. These items reflect the gradual expensing of long-term assets, but they can distort the picture of a company's immediate cash-generating ability.

For this reason, investors should never analyze the income statement in isolation. It must be cross-referenced with the cash flow statement to confirm that reported earnings are backed by actual cash. This comprehensive approach provides a more robust and reliable assessment of a company's true financial performance.

The preparation of financial statements is governed by a set of accounting standards to ensure consistency and comparability. The two dominant frameworks used globally are:

An awareness of these standards is important for investors analyzing companies from different jurisdictions, as the reporting methodology can affect key financial metrics.

Publicly traded companies are required to prepare and release their income statements on a quarterly and annual basis.

EBIT stands for Earnings Before Interest and Taxes, which is another term for operating income. EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. EBITDA adds back the non-cash expenses of depreciation and amortization to EBIT, providing a proxy for a company's operating cash flow.

Net income is fundamentally important because it represents the total profit available to a company's shareholders. It is the basis for calculating earnings per share (EPS) and is a key driver of a company's stock price and valuation over the long term.