Finance Terms

What are Central Banks?

*Videos are not yet available for all Finance Terms.

See video transcript

Central banks are the institutional cornerstones of a country's financial system. These powerful entities are responsible for architecting and implementing monetary policy, with the overarching goal of fostering a stable and prosperous economic environment. Their decisions have profound and immediate consequences for financial markets, influencing everything from the interest rate on a personal loan to the valuation of global stock indices.

The core mission of a central bank is typically multifaceted, balancing several critical objectives to ensure economic equilibrium. This includes maintaining price stability by controlling inflation, supporting maximum sustainable employment, and ensuring the overall stability and resilience of the financial system. For investors, a clear, analytical understanding of how central banks operate is not merely academic; it is essential for navigating the complexities of modern financial markets and making informed investment decisions.

Central banks operate with a mandate to manage the monetary affairs of a nation or a group of nations. While specific responsibilities can vary, their primary functions are universally directed toward achieving macroeconomic stability.

These core objectives are threefold:

To achieve these goals, central banks operate with a degree of political independence. This autonomy is crucial as it allows them to make technically sound, long-term policy decisions free from short-term political pressures that might otherwise lead to inflationary policies.

Central banks have a sophisticated toolkit at their disposal to steer the economy. These instruments are designed to influence the money supply, credit conditions, and overall liquidity in the financial system.

The primary monetary policy tools include:

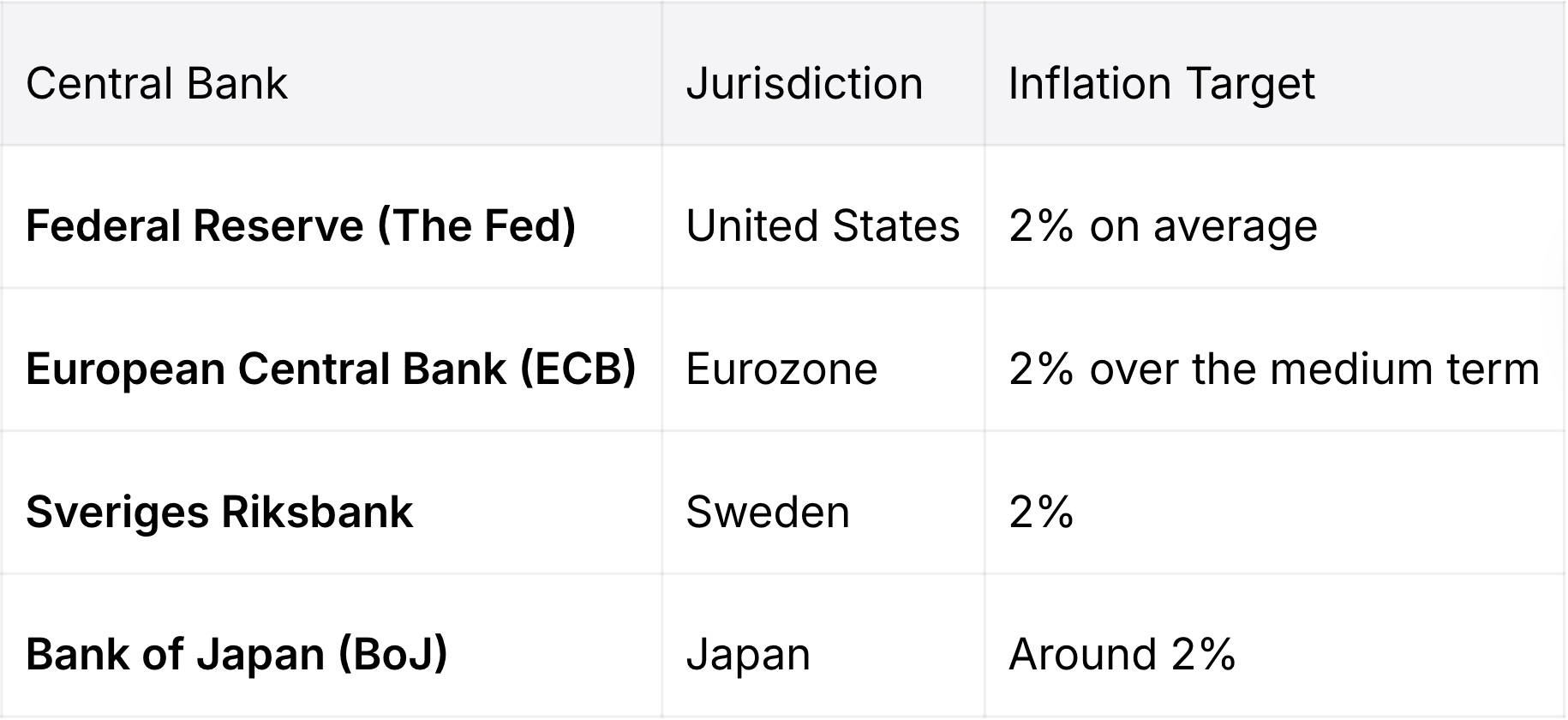

While the foundational principles are similar, central banks around the world adapt their policy frameworks to their specific economic realities. Each major central bank operates with a clearly defined inflation target, which anchors public expectations and guides its policy decisions.

These institutions, while independent, often act in a coordinated fashion, particularly during periods of global financial stress. However, their policy paths can diverge based on domestic economic performance, leading to shifts in global capital flows.

The decisions made by central banks have a direct and powerful impact on all asset classes. Investors and financial analysts meticulously parse every statement, press conference, and data release from central banks to anticipate future policy moves.

When a central bank tightens monetary policy by raising interest rates, the effects are widespread:

Conversely, when a central bank loosens policy by cutting rates, it generally stimulates the economy. Borrowing becomes cheaper, which can boost corporate investment, consumer demand, and asset prices. However, excessively loose policy carries the risk of fueling inflation and creating speculative asset bubbles.

The task of a central banker is fraught with challenges. They must navigate a complex trade-off between controlling inflation and supporting employment. The recent global tightening cycle of 2022–2023, initiated to combat a post-pandemic surge in inflation, provides a clear illustration of these difficulties. Raising rates aggressively risked triggering a recession, but failing to act would have allowed inflation to become entrenched.

Central banks also face criticism regarding:

The primary role is to conduct monetary policy to achieve macroeconomic stability, which centrally involves maintaining stable prices (controlling inflation) and supporting maximum sustainable economic growth and employment.

They primarily combat inflation by tightening monetary policy. This involves raising benchmark interest rates, which increases the cost of borrowing and reduces overall demand in the economy. They may also reduce the money supply through open-market operations.

Investors monitor them because their policy decisions have an immediate and significant impact on the value of financial assets, including currencies, bonds, and stocks. A change in interest rate expectations can move global markets in seconds.

Most major central banks are structured to be legally independent of direct government control. This independence is designed to prevent short-term political objectives from interfering with the bank's long-term mandate of ensuring economic and price stability.